**What is Open Banking?**

Open Banking is a financial framework that allows banks and third-party providers to securely share banking data through APIs, giving consumers more control over their financial information. This open access fosters innovation, as fintech companies can develop new products and services built on real-time financial data.

**How do Open Banking APIs work?**

Open Banking APIs provide standard interfaces for securely sharing financial data, such as bank account transactions, balances, and payment information. With customer authorization, these APIs enable third-party services to access and process financial data, fueling innovative solutions like budgeting apps, payment solutions, and investment platforms.

**Why is PSD2 significant for Open Banking?**

PSD2 (the Second Payment Services Directive) is a major European regulation mandating that banks safely share customer data with authorized third-party providers via standardized APIs. This directive accelerated Open Banking across Europe, sparking a wave of fintech innovation and expanding consumer choice by creating a more level playing field for financial institutions.

**What are the main benefits of Open Banking for consumers?**

Open Banking helps consumers quickly compare banking services, access personalized financial products and manage their finances more effectively. Streamlined account-switching, faster payment processes, and personalized budgeting tools are frequent advantages, making it easier for customers to find better interest rates, reduce fees, and receive tailored financial advice.

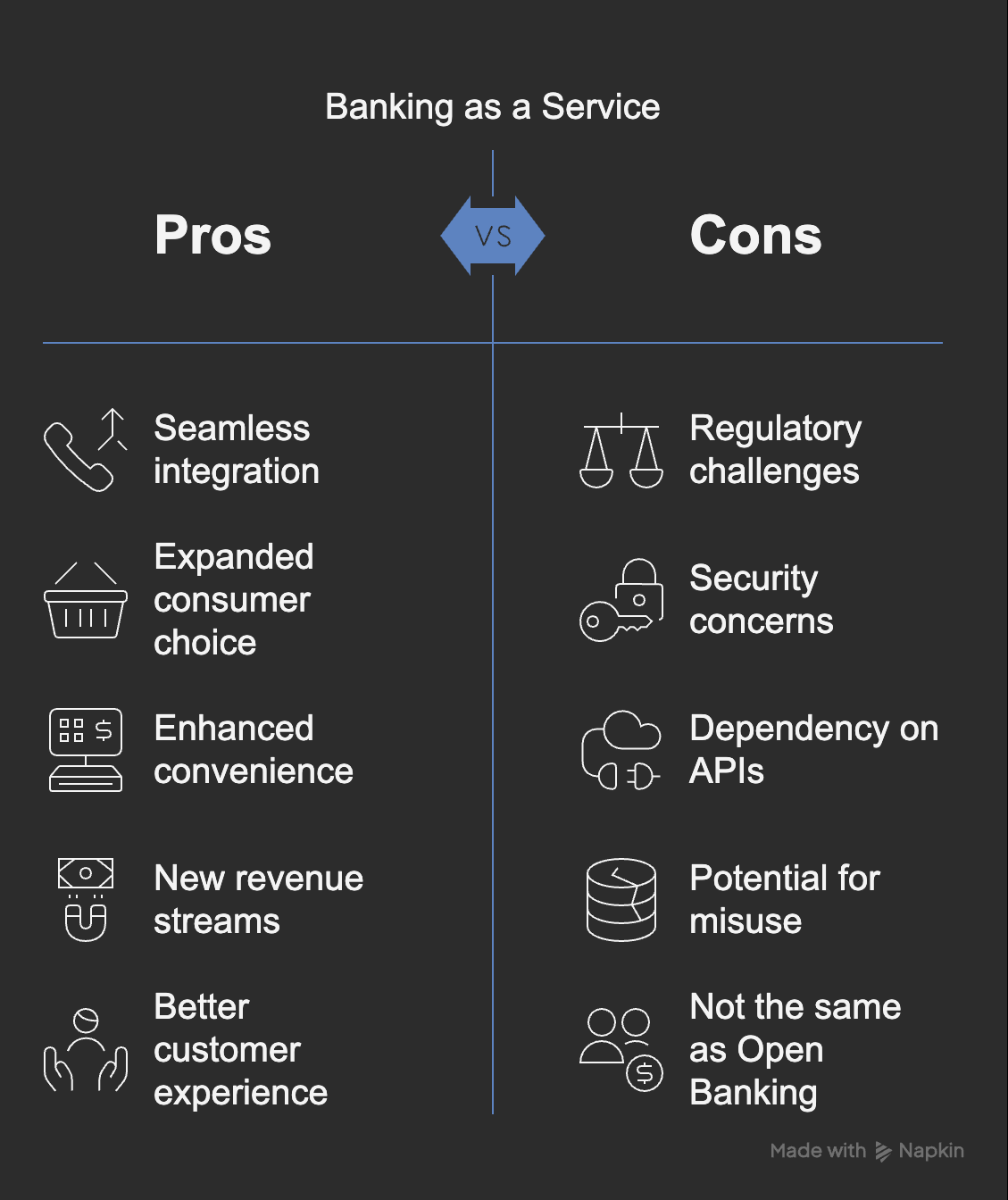

**How does Banking as a Service (BaaS) differ from Open Banking?**

Although both rely on APIs, BaaS focuses on banks providing their core banking services (like payment processing or loan issuance) to third parties, letting them embed those services into their own products. Open Banking, on the other hand, centers on sharing financial data with authorized third parties. Essentially, BaaS offers banking functions, while Open Banking offers data access.

**What security measures protect customer data in Open Banking?**

Open Banking relies heavily on secure protocols such as OAuth 2.0, TLS encryption, and strong customer authentication. Banks and fintech providers use multi-factor authentication, tokenization, and real-time fraud detection systems, ensuring financial data is encrypted before and during transfer, and access is granted only with explicit user permission.

**Are there Open Banking regulations in the United States?**

Yes. While the U.S. lacks a single, centralized Open Banking mandate like PSD2 in Europe, regulations proposed by the Consumer Financial Protection Bureau (CFPB) emphasize data portability and give consumers more control over their financial data. Voluntary guidelines and interagency collaboration help shape how Open Banking evolves across the country.

**How do Payment APIs help businesses under Open Banking?**

Payment APIs facilitate direct account-to-account transfers, often saving on processing fees charged by traditional methods like credit cards. By integrating real-time, secure payment capabilities, businesses can boost conversion rates, lower fraud risk, reduce chargebacks, and often receive instant settlement of funds.

**What is the role of fintech startups in Open Banking?**

Fintech startups leverage secure Open Banking APIs to build consumer-facing apps and services that deliver personalized budgeting, faster payments, and advanced financial insights. By accessing real-time banking data, these companies can rapidly develop and iterate new solutions that challenge traditional banking norms and enrich the financial ecosystem.

**How do global regulations impact Open Banking implementation?**

Different regions adopt various regulatory models—Europe uses PSD2, Australia has the Consumer Data Right (CDR), and the U.S. follows a more decentralized approach. Each framework addresses security, data privacy, and customer empowerment in its own way, influencing how quickly new banking solutions can be launched and integrated.

**Which standards support security and interoperability in Open Banking?**

Standards such as the Financial-grade API [(FAPI) from the OpenID Foundation](https://openid.net/wg/fapi/)(FAPI) from the OpenID Foundation and the Berlin Group's NextGenPSD2 framework define secure authentication, authorization, and data exchange processes. These standards help ensure consistency and reliability for banks, fintechs, and consumers, promoting widespread adoption of Open Banking solutions.

**What does the future hold for Open Banking?**

Open Banking is expanding into broader "Open Finance," integrating services like insurance, investments, and lending under a unified digital infrastructure. Emerging technologies, including AI and blockchain, will enable more personalized products and reduce friction in accessing financial services. As consumer trust and regulatory frameworks mature, collaboration between traditional banks and fintechs will continue driving new business models and enhanced user experiences.