Core API Services Powering Financial Innovation

Open Banking is revolutionizing how consumers interact with financial services by offering them more control and choice over their financial data. It allows consumers to easily compare services and user experiences across different financial organizations, making financial management more accessible and personalized via several core functionalities:

- Account Information Services (AIS): These APIs allow consumers to securely share account balances and transaction details with third-party applications. They enable tools such as budgeting apps and financial dashboards to provide enhanced insights.

- Payment Initiation Services (PIS): By facilitating direct payments from user accounts through third-party platforms, these APIs offer alternatives to traditional card payments, reducing costs and processing times.

- Data Aggregation Services: These specialized interfaces consolidate financial information across multiple institutions, giving users a comprehensive view of their finances in a single location.

Open Banking Benefits for Consumers & Businesses

The obvious benefit of Open Banking to the customer is rather like financing being sold to a new car buyer. If the customer is offered an “ideal” banking product, such as financing for a new purchase at a significantly better interest rate in the showroom, being able to seamlessly take up that offer clearly has a positive impact on the overall customer experience.

Other benefits of Open Banking for consumers include simplifying the process of obtaining new credit and debit cards, enabling budgeting tools to more easily track and manage spending, and making switching between banks a (relatively) joyful experience.

Payment APIs

Open Banking’s payment APIs present many advantages over other payment methods for businesses, including better conversion rates and acceptance rates, and an overall ease of experience. Payment APIs also unlock lower fees for merchants — who are regularly stuck with fees and costs when accepting credit cards. Payment APIs also eliminate chargebacks (which can hurt companies) and see funds settled instantly (not over days).

A rather recent addition to the payment experience comes in the form of “Buy Now, Pay Later” offerings, which seem to be a real hit with the younger demographic. Integrating these newer payment methods into existing product purchasing journeys helps provide a modern, more relevant experience across a broader range of customers and their payment preferences.

Data APIs

Data that can be shared in Open Banking might include phone number, email and address, balance information, product rates, fees, features, and transaction details. Data gathered through Open Banking APIs brings many benefits to businesses, including getting a better picture of customer needs to deliver a better customer experience, improved customer onboarding, and reduced administrative work required around compliance processes. Secure, governed access to data like this goes a long way to streamlining the onboarding of new offerings for customers.

Industry Standards Ensuring Compatibility and Security

To ensure interoperability, security, and scalability, Open Banking APIs adhere to established industry standards:

- Financial-grade API (FAPI): Developed by the OpenID Foundation, FAPI ensures strong authentication and authorization protocols for secure financial data exchange, addressing the unique security requirements of banking transactions.

- Berlin Group's NextGenPSD2: Widely implemented across Europe, this standard streamlines integration between banks and fintech companies, simplifying integration processes and creating a more unified technological approach.

Security-First API Management

Robust API management is critical for Open Banking. Key practices include:

- Strong Authentication Protocols: Secure protocols like OAuth 2.0 and OpenID Connect ensure multi-layered verification before granting access to financial data.

- Traffic Control Mechanisms: Strategic rate limiting prevents system overload and potential security breaches by controlling API request volumes.

- Comprehensive Monitoring: Real-time performance tracking and detailed activity logs support both security auditing and system optimization.

Organizations often deploy specialized API management platforms like Kong Gateway to maintain operational efficiency while meeting stringent security and regulatory requirements. By leveraging these platforms, financial institutions ensure robust and scalable management of Open Banking APIs, optimizing scalability and security while maintaining robust operational efficiency.

Security, Innovation, and Transformation: Navigating the Open Banking Landscape

Securing the Financial Data Ecosystem

As APIs facilitate unprecedented access to sensitive financial data, security and privacy have become non-negotiable priorities. The cornerstone of Open Banking security is explicit user authorization. Consumers must have a clear understanding of what financial data is shared, with whom, and for what purpose. Advanced techniques like TLS encryption, tokenization, and strategic anonymization provide critical protection layers throughout the data lifecycle.

Proactive Risk Management

Financial institutions are deploying Strong Customer Authentication (SCA) with sophisticated multi-factor verification, including advanced biometrics, to significantly reduce fraud exposure. AI-powered fraud detection systems leveraging machine learning continuously monitor transactions to detect and neutralize suspicious activities before they become threats.

Cultivating Trust Through Openness

Building trust requires clear communication about data usage, robust privacy policies, and strict compliance with regulations such as GDPR in Europe. Organizations winning in the Open Banking space prioritize transparency, accountability, and a customer-first approach to sustain trust.

Innovative Business Models Reshaping Finance

Open Banking paves the way for innovative business models and new revenue streams. Forward-thinking banks now offer tiered API services featuring advanced capabilities, enhanced data access, and premium usage allowances for fintech partners and enterprise clients, creating valuable new revenue channels.

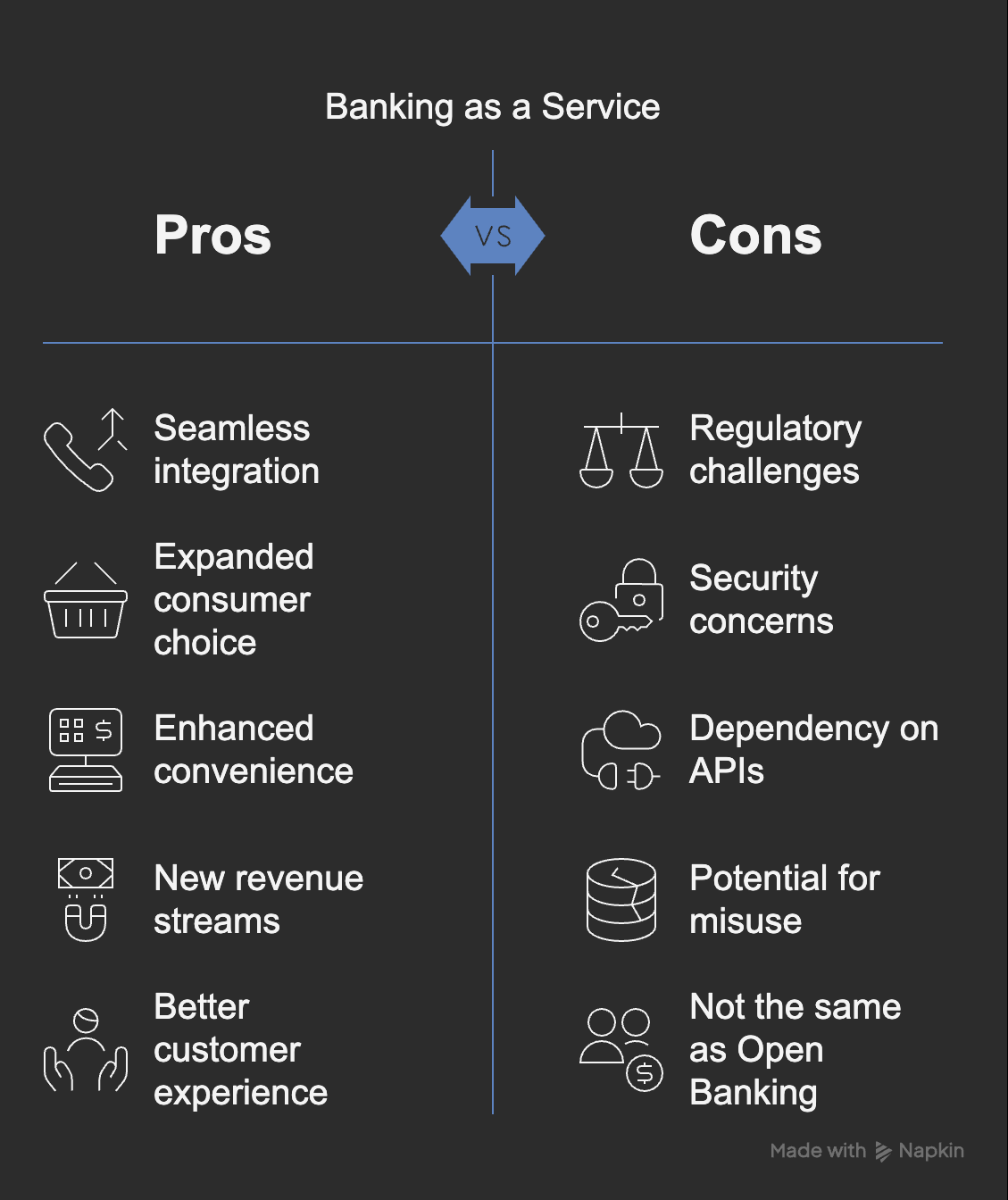

Financial Services as Integrated Components

Through Banking as a Service (BaaS), financial institutions can embed their core services directly into non-banking platforms, unlocking access to entirely new customer segments. Transaction fees, subscription models, and strategic revenue-sharing arrangements provide multiple paths to monetization.

Value Creation Through Collaboration

Strategic partnerships between established banks, nimble fintech startups, and technology providers help mitigate innovation costs and accelerate time-to-market. Joint ventures, co-branded solutions, and white-labeled offerings exemplify this partnership-driven approach.

Beyond Banking: The Future of Open Finance

The future vision expands beyond banking to a broader "Open Finance" ecosystem, integrating investments, insurance, pensions, and mortgages. Emerging technologies like AI, blockchain, and decentralized finance (DeFi) will further revolutionize financial services, driving efficiency, transparency, and inclusivity. That being said, in order to have a successful Open Banking adoption plan, it is vital to have strategic planning, robust technical execution, and agile team structures. Executive leadership must strategically evaluate partnership opportunities and technology investments, while development teams focus on API security, compliance, and scalability.

Embracing the Open Banking Future

Open Banking represents a fundamental paradigm shift that places consumers at the center of the financial ecosystem. To thrive in this new landscape, businesses must innovate boldly, collaborate strategically, and remain steadfastly customer-focused. By embracing regulatory changes and leveraging emerging technologies, organizations can unlock immense opportunities in this interconnected financial ecosystem.

The Open Banking revolution is underway—creating unprecedented opportunities for those ready to build a more connected, innovative, and inclusive financial future. Let's embark together on this exciting journey!

Open Banking FAQs

What is Open Banking?

Open Banking is a financial framework that allows banks and third-party providers to securely share banking data through APIs, giving consumers more control over their financial information. This open access fosters innovation, as fintech companies can develop new products and services built on real-time financial data.

How do Open Banking APIs work?

Open Banking APIs provide standard interfaces for securely sharing financial data, such as bank account transactions, balances, and payment information. With customer authorization, these APIs enable third-party services to access and process financial data, fueling innovative solutions like budgeting apps, payment solutions, and investment platforms.

Why is PSD2 significant for Open Banking?

PSD2 (the Second Payment Services Directive) is a major European regulation mandating that banks safely share customer data with authorized third-party providers via standardized APIs. This directive accelerated Open Banking across Europe, sparking a wave of fintech innovation and expanding consumer choice by creating a more level playing field for financial institutions.

What are the main benefits of Open Banking for consumers?

Open Banking helps consumers quickly compare banking services, access personalized financial products and manage their finances more effectively. Streamlined account-switching, faster payment processes, and personalized budgeting tools are frequent advantages, making it easier for customers to find better interest rates, reduce fees, and receive tailored financial advice.

How does Banking as a Service (BaaS) differ from Open Banking?

Although both rely on APIs, BaaS focuses on banks providing their core banking services (like payment processing or loan issuance) to third parties, letting them embed those services into their own products. Open Banking, on the other hand, centers on sharing financial data with authorized third parties. Essentially, BaaS offers banking functions, while Open Banking offers data access.

What security measures protect customer data in Open Banking?

Open Banking relies heavily on secure protocols such as OAuth 2.0, TLS encryption, and strong customer authentication. Banks and fintech providers use multi-factor authentication, tokenization, and real-time fraud detection systems, ensuring financial data is encrypted before and during transfer, and access is granted only with explicit user permission.

Are there Open Banking regulations in the United States?

Yes. While the U.S. lacks a single, centralized Open Banking mandate like PSD2 in Europe, regulations proposed by the Consumer Financial Protection Bureau (CFPB) emphasize data portability and give consumers more control over their financial data. Voluntary guidelines and interagency collaboration help shape how Open Banking evolves across the country.

How do Payment APIs help businesses under Open Banking?

Payment APIs facilitate direct account-to-account transfers, often saving on processing fees charged by traditional methods like credit cards. By integrating real-time, secure payment capabilities, businesses can boost conversion rates, lower fraud risk, reduce chargebacks, and often receive instant settlement of funds.

What is the role of fintech startups in Open Banking?

Fintech startups leverage secure Open Banking APIs to build consumer-facing apps and services that deliver personalized budgeting, faster payments, and advanced financial insights. By accessing real-time banking data, these companies can rapidly develop and iterate new solutions that challenge traditional banking norms and enrich the financial ecosystem.

How do global regulations impact Open Banking implementation?

Different regions adopt various regulatory models—Europe uses PSD2, Australia has the Consumer Data Right (CDR), and the U.S. follows a more decentralized approach. Each framework addresses security, data privacy, and customer empowerment in its own way, influencing how quickly new banking solutions can be launched and integrated.

Which standards support security and interoperability in Open Banking?

Standards such as the Financial-grade API (FAPI) from the OpenID Foundation and the Berlin Group's NextGenPSD2 framework define secure authentication, authorization, and data exchange processes. These standards help ensure consistency and reliability for banks, fintechs, and consumers, promoting widespread adoption of Open Banking solutions.

What does the future hold for Open Banking?

Open Banking is expanding into broader "Open Finance," integrating services like insurance, investments, and lending under a unified digital infrastructure. Emerging technologies, including AI and blockchain, will enable more personalized products and reduce friction in accessing financial services. As consumer trust and regulatory frameworks mature, collaboration between traditional banks and fintechs will continue driving new business models and enhanced user experiences.